Table of Content

Talk to your lender to make sure you have all of the proper documentation needed to ensure you are the sole owner of the home you intend to purchase. Once the payee is active, you will be able toschedule paymentsto this payee. Once the information is added, you’ll need to activate the payee by selectingactivate payee nowand the method you’d like to receive the activation code. We dedicate our expert Home Loan Guides to work with you from start to finish.

For instance, if you put some of the cash that you saved toward paying off high-interest credit card debt, an interest-only mortgage can be a good financial management tool. A Home Equity Loan enables homeowners to borrow money that is secured by the equity they have in their home. The borrower pays interest and pays down the loan as soon as the money is borrowed. If a borrower opts for a cash-out refinance, they are essentially refinancing their current mortgage for more than what they currently so they can receive extra funds.

What is a home equity loan and how does it work?

Only some lenders require you to put money down, typically for those with poor credit. The process may temporarily cause a dip in your credit score due to the fact that applying will cause a hard credit pull. On top of that, your score could decrease due to the added account.

Take a look at the pros and cons of a home equity loan to see if applying for one makes sense for you. Determine whether a home equity loan is the right loan for you. When you have a home equity loan, you can use it to boost your finances. Take your time, though, to fully comprehend the pros and cons of the process. Borrowers have the advantage of having a mortgage broker’s network as their primary source of assistance.

All About Housing and Home Equity

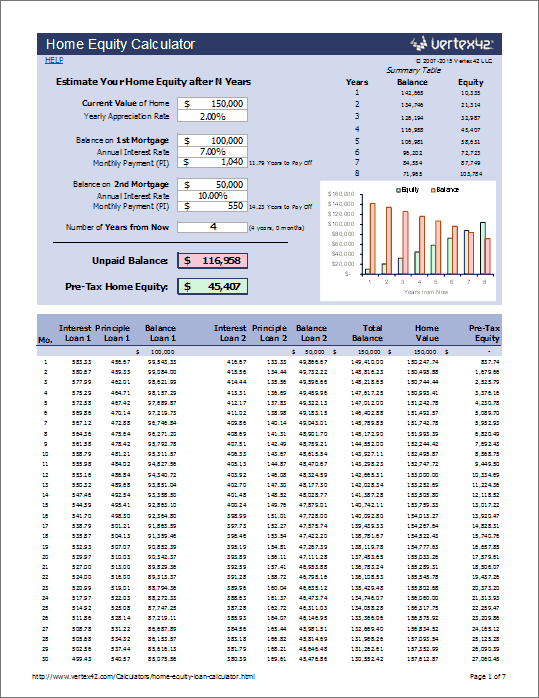

A home equity loan is a loan that is secured by the equity in your home. The equity is the difference between the appraised value of your home and the amount you still owe on your mortgage. If you have equity in your home, you may be able to refinance your home equity loan. Home equity loan is a good source of money for major projects and one-time expenses. Selling your home for a profit can mean a substantial windfall. Meantime, while you're living there, that gain is locked up, out of reach — unless you access the equity with a home equity loan or a home equity line of credit, known as a HELOC.

Read more about down payment requirements andsaving for a down payment. There are other factors lenders take into consideration beyond credit score, and it’s in the lender’s best interest to help you find a solution. Consistent payment history - For a home equity loan, a history of reliable payments on your mortgage or other debts is extremely important. It serves as proof that they can rely on you to make steady payments on this loan as well. Income rates - For most loans, the amount of income that you have will factor into whether or not you’re awarded the loan, as well as the amount that you receive. Some lenders charge different fees depending on the amount of the home equity loan, and some have zero fees for any home equity loans.

Personal Banking

These loans make your payments predictable whether you are funding a wedding or significant home renovation. A HELOC typically has a lower interest rate than credit cards and can be used for any type of purchase. Some common uses for a HELOC include home renovations, buying a second home or investment rental property, paying for college tuition, and paying-off high interest debt. It is most likely that you will be eligible for a loan if you have a credit score of at least 680 and an equity stake in your business. In terms of credit scores, the majority of lenders prefer borrowers with a credit score of 700 or higher. Homeowners with credit scores ranging from 622 to 679 may be approved.

The transaction will still be protected by multiple layers of security and zero liability for fraudulent purchases. You’ll work directly with us to resolve any issues or make changes to your loan, such as removing PMI or requesting mortgage relief. You can't pay accidentally—your card or device must be within 1- 2 inches of the terminal for the sale to take place. If you're not sure if your card has been lost or stolen, and would like toturn it off temporarily,you may do so using the card controls option in the mobile app. If you already have a card with Solarity, a new Contactless card will be automatically issued to you. Your bank or card issuer will verify your information and decide if you can add your card to Apple Pay.

For example, the bank does not state a maximum LTV or minimum debt-to-income ratio that borrowers must have, nor does it name FICO score requirements. You can get a small loan of up to $150,000 secured by the equity in your home here. It will have a maximum repayment period of 20 years, and you won’t even need to leave your home to get the money, as the bank accepts all applications online from any state. Unlike home equity lending, a personal loan is typically not secured by your house. That means it’s riskier for banks , and the interest rates are much higher as a result.

If you’re new to Solarity and wish to become a member, start here. If you’re already a member and would like to open additional accounts, start here. Solarity does not offer private party loans on vehicles, motor homes, travel trailers, campers, fifth wheels, boats and jet skis.

A reverse mortgage is made available by a lender in the form of a lump sum or monthly payments. A personal loan is a type of installment loan that is typically interest-only. If you’re looking for a short-term loan with a low interest rate, consider a 0% APR credit card. A home equity loan is a type of loan in which the borrower uses the equity of their home as collateral.

A HELOC has a borrowing limit just like a credit card, but unlike a credit card, a HELOC is established for a set amount of time called a “draw period”. During that draw period, you’re typically required to make interest-only payments each month on any outstanding balance. A home equity loan is where you borrow money from a bank or lender using your home as collateral.

As with a credit card, you only have to pay interest on the amount of credit you use. However, some lenders also set a mandatory minimum monthly payment. Most lenders will only agree to work with lenders whose score is above 650.

Taking out a home equity loan isn’t as quick or easy as applying for a new credit card. The process usually takes weeks, or sometimes months, as the bank looks over your application and credit history. Have you paid your current mortgage on-time or do you have missed or late payments? Lenders want to know you’re a reliable borrower before they approve the loan. Refinancing your mortgage could save you hundreds of dollars for your monthly mortgage payment and secure you tens of thousands of dollars in long-term savings.

No comments:

Post a Comment